Sign up to receive accounting tips, videos, news and webinar info before anyone else

Mailing Address

21750 Hardy Oak Blvd

Ste 104 PMB 63328

San Antonio, TX 78258-4946

(760) 697-1033

As your company’s finances grow and become more complex, it is important to understand “what is a controller?” in order to hire and delegate responsibilities appropriately.

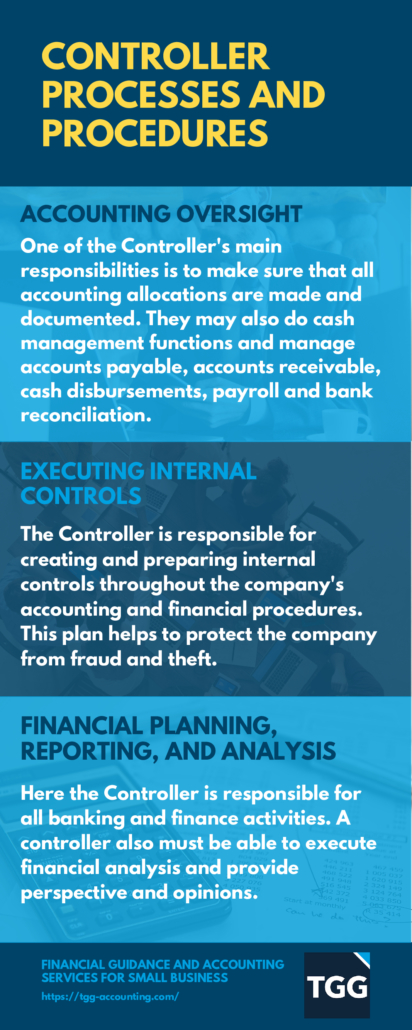

What does a controller do in a business? Controllers are responsible for providing oversight and management to the organization’s financial reporting, budgeting, forecasting, accounting processes, compliance with legal regulations, and other financial activities. Additionally, controllers may be called upon to manage the organization’s cash flow and develop financial strategies in order to maximize profits. Controllers are also responsible for measuring performance against budgeted targets and providing advice regarding operational risks or opportunities.

Controllers and CFOs both oversee the financial operations of an organization, however their roles are very different. The responsibilities of a controller typically include day-to-day accounting activities such as accounts payable/receivable, payroll, budgeting and cash flow management. In contrast, a CFO (Chief Financial Officer) is involved in higher level decisions such as strategic planning, capital investments, and mergers/acquisitions. A CFO will be more involved in the company’s overall performance and financial health than a controller would be.

Another distinction to make in hiring is between an accounting manager vs controller. An accounting manager is responsible for managing the daily activities of an organization’s accounting department. They may oversee bookkeepers, accounts payable/receivable clerks, payroll staff and other individuals within the department. An accounting manager will typically report to a controller or CFO, and they are not responsible for higher-level tasks such as strategic or capital planning. So, if you are looking to understand “what does an accounting controller do?,” they would likely manage the accountants for the company.

Your Controller should not be doing data entry. The Controller’s main job responsibility is to manage the accounting department from a high-level. Compared to your Bookkeeper, Staff Accountant and/or Accounting Manager, the Controller is focused on ensuring the accuracy of the financial statements. Controllers are also responsible for taking the financial information, interpreting the results and communicating them to management and non-accountants in a way that they can understand. A Controller will also suggest improvements to achieve the goals for the business. Financial Controllers report to the Chief Financial Officer (CFO). Their day-to-day duties include the preparation of operating budgets, overseeing financial reporting, and performing essential functions related to payroll.

The most important job of a Controller is to “tell the story” of what’s going on in the business. They communicate the story through graphs, charts and pictures to show where the business is and where is has the potential to go. In order to do this successfully, the Controller must have a thorough understanding of the goals for the business so they can determine the most important aspects of the financial package to highlight. The Key Performance Indicators (KPIs) and ratio analysis, including gross profit metrics, are areas the Controller will focus their efforts.

The Controller is also in charge of internal controls and takes responsibility for fraud prevention within a company. They create and prepare internal control procedures for their company for both the financial and accounting departments. Controllers are tasked with reducing risk in a business through compliance, regulatory reporting and safeguarding assets. The strategies that the Controller creates to minimize financial risk are based on the goals for the business.

In most, if not all accounting departments, the Controller will report to the CFO. They will also manage and support the Accounting Manager and hold them accountable for producing accurate and timely financial information. The data must be accurate in order for the Controller to analyze it and fulfill their job responsibilities. Once the Controller has signed off on the financial package, they send it to the CFO for them to present to management and key stakeholders in the business.

Now that you understand “what is a controller,” you also need to understand how to find a qualified one. When hiring a controller, it is important to look for an individual who has extensive experience in the fields of accounting and finance. A controller should have knowledge of Generally Accepted Accounting Principles (GAAP) as well as expertise in budgeting, forecasting, financial analysis and strategic planning. Especially if you need them to manage your accounting team, they should possess strong leadership skills and be comfortable working in a fast-paced environment.

Answering the question “what does a controller do in a business?” also informs the educational background to look for in candidates resumes. Ideally, the controller should have a bachelor’s degree in Accounting or Finance and may even have an MBA in addition to their relevant certifications. Many larger companies also prefer controllers with CPA (Certified Public Accountant) credentials as well as experience with accounting software.

Ultimately, the role of the controller is to ensure that the business’s financial activities and financial reporting are carried out in an efficient and accurate manner. In a word, the answer to “what is a controller?” is accuracy. The risks of not having a controller include the potential for financial mismanagement, inaccurate reporting, and inadequate forecasting. Without a controller to provide oversight and guidance, there is a much higher risk that errors may occur which could lead to significant financial losses or compliance issues.

All growing businesses need to be able to articulate an answer to the question “what is a controller in finance?” because as they grow, their accounting needs typically intensify. Any businesses with complex accounting requirements may find it beneficial to have either a full time or fractional controller. Businesses that require tight financial control, such as manufacturing or healthcare organizations, often rely heavily on controllers to provide the necessary oversight and should have a full time controller.

Companies that are growing rapidly and looking to scale may also benefit from having a fractional controller, a controller who works on an as-needed basis and often works remotely, on board as they can help ensure that the finances remain organized and accurate.

At TGG, we allocate a 4-person team to every client, consisting of a CFO, a Controller, an Accounting Manager, and a Staff Accountant to make sure the accounting is being done at the appropriate levels. Is your Controller doing data entry? If so, reach out to us today for a free 30-minute consultation so we can partner with your existing staff and get your accounting department on the right track!

This post was reviewed by our team of accounting and financial experts. TGG’s mission is to make business owners’ lives better through excellent financial management. We strive to provide the most up-to-date and objective information on accounting-related topics so our readers can make informed decisions based on factual content. All posts undergo a review process with at least one member of our Leadership Team to ensure accuracy.

This post contains trusted sources. All references are hyperlinked at the end of the article to take readers directly to the source.

How to Create Contingency Plans for Supply Chain Disruptions

How to Create Contingency Plans for Supply Chain Disruptions