Sign up to receive accounting tips, videos, news and webinar info before anyone else

Mailing Address

21750 Hardy Oak Blvd

Ste 104 PMB 63328

San Antonio, TX 78258-4946

(760) 697-1033

At TGG we have started Bonfire Chats, webinars created to answer your questions surrounding today’s environment, and what you may need to know in the coming weeks. Last week, we discussed the Main Street Lending Program, and why it may be beneficial for you.

The Main Street Lending Program began in April, and has seen trouble gaining traction. Unlike the SBA PPP, the MSLP works with larger businesses and can provide funding for businesses in need during this uncertain time. This program could be one of the most beneficial programs for businesses today if used properly.

Matt Garrett, CEO & Founder of TGG Accounting and Bruce Lambright, one of TGG’s CEOs discuss what the Main Street Lending Program can do for you. Here are a few of the frequently asked questions.

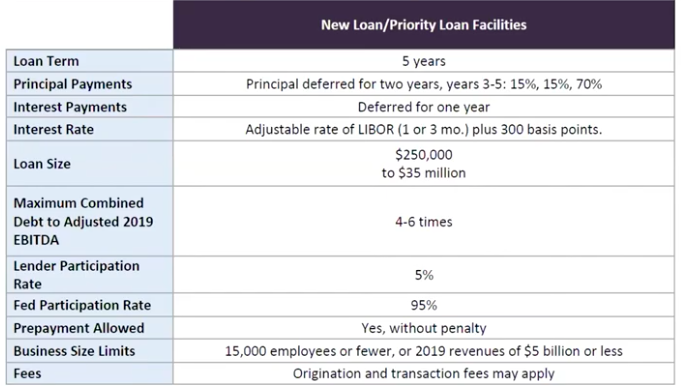

Unlike the SBA PPP, the MSLP is a loan, not a grant. The loan details are listed here:

The FED extended the deadline for the MSLP from September 30, 2020, to December 31, 2020. Unlike other loan programs created to help business owners through this uncertain time, the MSLP loan is based on your EBITDA (net income with interest taxes, depreciation, and amortization), and is affected by the multiplier.

There are a few different items accepted as EBITDA adjustments, depending on your bank. These adjustments can affect your loan size, so it is important to look at multiple options to ensure your business is getting the best offer.

The MSLP does not technically require a personal guarantee when taking out a loan, most banks will require it. A personal guarantee is a way for the bank to ensure they receive their payments. They do this by requiring the person taking out the loan to pledge personal assets to back the loan.

Priority loans under the MSLP are able to refinance debt at the onset of the loan. This is calculated by the EBITDA x multiplier – current debt. The debt would be loan lines of credit, potentially mortgages, idle loans from the SBA or PPP, if you can prove you’re on track for full forgiveness. Accounts payable and credit card debt is not included in this calculation.

Main street loans can be junior to any other debt. Refinancing debt can be done under the priority loan but you must do it at the time you originated the loan. Remember, it can’t be from the same bank!

The best way to maximize your MSLP loan is to include all possible EBITDA adjustments. For example, if you settled a lawsuit last year, it would be a one-time expense and could be added back. However, your meals would be considered recurring. Be realistic about your adjustments as you work to receive the most you can from this loan.

This will vary from bank to bank, different banks are looking at them very differently. View these loans as you would with any commercial loan positioning. What are your weaknesses? How can you make them look less impactful or like a strength?

Banks are using the same criteria they normally use to underwrite loans. This includes the strength of the balance sheet, your cash flow statements, and your business’ past performance. Be sure to have this organized before you look to take out a loan.

This will vary depending on the bank you are looking to take out a loan with. Now, most banks will see this as an added benefit, so you can use this as a bargaining tool. With this loan program, banks have to do the full underwriting process, and are giving 95% of that business to the FED. With these loans bringing in such limited business for the bank, they likely want the client to have a relationship with them for the future.

Both small, local banks are participating, as well as large, national banks. The main difference in taking out a loan with a larger bank is that there will likely be a limit put on the loan size you can take out. In larger banks, loans under 10 million will likely not be accepted. Some banks won’t give out loans beyond Southern California, or to restaurant owners.

To begin searching for a bank, narrow your list of banks down to fit the parameters of your specific business. Be sure you present your business’ information in an organized manner. Before you go to the bank, consider questions the bank might ask. How is your new idea going to be different from your historical performance? How will your restaurant look when the economy comes back? Consider these questions and be ready to answer them when you go to the lender.

As long as you are operating within the guidelines of the bonding agency and industry, taking out a loan with the MSLP will not likely be an issue. Construction is qualified. You must ensure your business is an eligible business. Real estate holding companies and private equity held companies are not typically eligible.

Under the MSLP, members of the organization that received more than $425,000 in 2019 are limited to $425,000 moving forward. There are loopholes that can get you up higher, but those are a bit more complicated. For more information contact Bruce.

As far as distributions go, distributions were not originally allowed for the term of the loan plus one year after. Recently, they made a change to allow pass-through organizations to take distributions to pay the tax generated by the business.

Remember to do everything in good faith, as many business owners have been charged with fraud for misusing the funds.

Different lenders have different levels of expertise, some may suggest different programs to help your business succeed. The MSLP does not require collateral, but bankers likely require it. The SBA may be more advantageous for some businesses but it requires collateral. Businesses may also want to include commercial debt instruments that are typically around. As a business owner, pursue as many avenues as possible to get your business the best deal.

Another thing to consider is forecasting, By forecasting your cash flow you will be better equipped to see where your business may be headed, and what you may need in the future.

The list provided by Boston FED is a limited list, with only the banks who allow their names to appear on the list. There are banks not on that list that are lending. The banks on the Boston FED list are likely overrun with inquiries and have been slower to respond.

Contact Bruce Lambright (bruce.lambright@tgg-accounting.com) if you have any questions regarding the MSLP.

As you can see, the Main Street Lending Program is a bit more complicated than we originally thought. The best thing you can do to prepare to apply for a loan is to get organized, search for multiple offers, consider all of your options to prepare for what may happen with the future of the economy. Download TGG’s Main Street Loan Organizer Toolkit now!

Enjoy this Bonfire Chat? Email info@tgg-accounting.com to suggest potential topic ideas or if you have any questions.

This post was reviewed by our team of accounting and financial experts. TGG’s mission is to make business owners’ lives better through excellent financial management. We strive to provide the most up-to-date and objective information on accounting-related topics so our readers can make informed decisions based on factual content. All posts undergo a review process with at least one member of our Leadership Team to ensure accuracy.

This post contains trusted sources. All references are hyperlinked at the end of the article to take readers directly to the source.

Your Definitive Guide to Cash Flow Forecasting

Your Definitive Guide to Cash Flow Forecasting